Ostrum Asset Management, one of the asset managers of the Natixis group, recently published its new coal policy. This is based on the recommendations of NGOs as well as the ACPR and AMF report and is aligned with best market practices. Ostrum thus becomes the 18th French financial actor to adopt a robust exit policy from the sector. Reclaim Finance calls on the other affiliates of Natixis Investment Manager, such as DNCA, Loomis and Ossiam, as well as the Natixis bank and Natixis Assurances, to show the same ambition

1. What’s new

Ostrum has gone beyond the policy announced by the Natixis group in October 2020 and extended it by adding the following elements:

- exclusion of companies planning to develop new coal infrastructure;

- divestment from companies that are developing new coal projects and which derive more than 25% of their income from coal as of this year, rather than waiting until 2022;

- divestment from companies which produce more than 20MT of coal per year or which operate more than 10GW of coal-fired power generation capacity;

- a commitment to no longer invest, as of January 1, 2022 in companies that have not adopted by then a credible plan for phasing out coal, aligned with the ultimate objectives of total exit from the sector by 2030 in OECD and by 2040 elsewhere;

- regarding implementation, Ostrum is committed to applying the policy to open funds and to working towards a gradual application of the policy to dedicated funds or mandates.

2. Our analysis

Ostrum is complementing the measures announced in October 2020 with essential elements for a sound coal exit policy. First of all, the immediate exclusion, without delay, of all companies planning new coal projects is a vital step for any financial actor wishing to align their practices with climate science.

Ostrum’s actions thereby recognize the incompatibility of any new coal project with the available carbon budget, while also announcing its commitment to reduce to zero its exposure to coal on a timeline aligned with the 1.5 ° C target.

In addition, Ostrum takes into account the recommendations of the ACPR and the AMF by specifying the database it will use to guide the application of the measures taken, namely the Global Coal Exit List – a benchmark of quality – and is also adopting exclusion criteria based on the absolute exposure of companies to coal. Thus, the 25% exclusion threshold is complemented by an exclusion of the largest producers of coal or electricity from coal.

Companies breaching the thresholds of 20MT and 10GW will be divested within six months. It should be noted that while Ostrum announces that it will revise these thresholds at the end of 2021, those applied for the moment are higher than those retained by the 2020 GCEL.

The metric used to exclude companies deriving more than 25% of their income from coal-powered electricity production does however remain problematic and less relevant than the share of coal-powered electricity production, which is more indicative of the company’s actual climate impact.

In another very positive development, Ostrum is committed to pushing companies active in the coal sector and remaining in its portfolio to take action now to foresee and anticipate the necessary steps relating to their exit from the sector. If the measures to be found in the exit plans would benefit from being specified, Ostrum declares that it wants to ensure their credibility and alignment with climate objectives and sets a clear deadline: the end of 2021. Companies that fail to produce these exit plans will no longer be able to benefit from new investments after January 1, 2022.

Finally, while this new policy will rapidly apply to all open funds managed by Ostrum, and will be applied by default to new dedicated funds and mandates, the principal challenge lies in the application to dedicated funds and existing mandates. These represent around 85% of assets under management. Ostrum is committed to approaching its customers gradually to offer them the policy, but does not specify the timetable or whether contracts with customers resistant to any coal exclusion will be renewed. The policy does not apply to index management, but assets managed in this way represent only a very small portion of total assets.

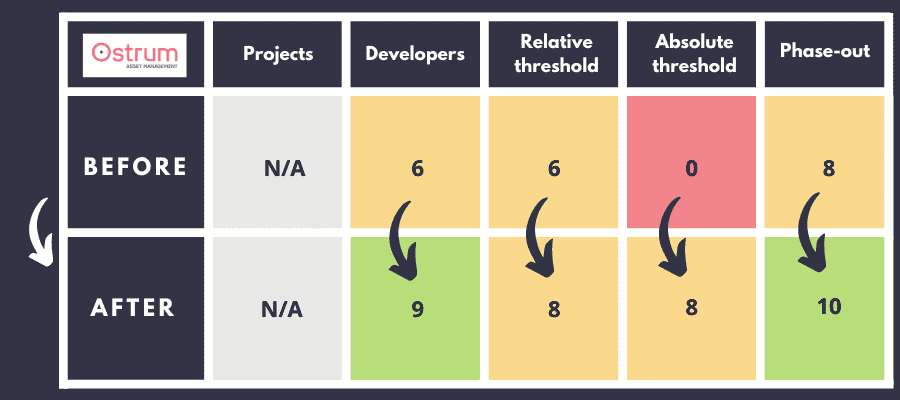

Ostrum AM’s Scores in the Coal Policy Tool

This table presents the coal scores of Ostrum AM based on 5 criteria of the Coal Policy Tool

3. Conclusion

Ostrum is adopting the policy expected from Natixis in October, namely a policy consistent with the climate emergency and with the leadership that Natixis had shown in 2015 on coal before being overtaken by its peers. Reclaim Finance calls on the other affiliates of Natixis Investment Manager, such as DNCA, Loomis and Ossiam, as well as the Natixis bank and Natixis Assurances to show the same ambition.

As for Ostrum, 2020 must be geared towards shareholder engagement with companies like Engie, which will need to be convinced to adopt plans to quit coal based on closing assets and replacing them with renewables. Conversion to gas or biomass must be avoided, otherwise one problem will be replaced by another. Finally, Ostrum will need to tackle unconventional gas and oil, starting by demanding portfolio companies stop developing new oil sands, shale gas and oil and Arctic-based projects, be they production or transportatio